Change the chart title and data settings.

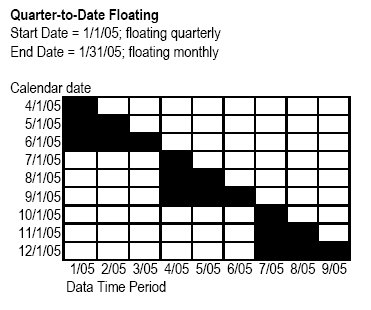

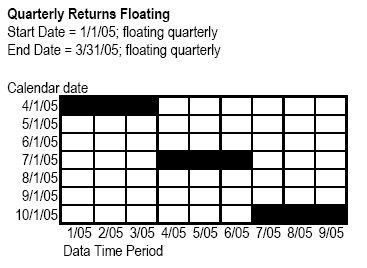

You can float the start and end dates for your analysis on a monthly, quarterly, semiannually, or yearly basis and also build lag time into the calculation. See below for some examples of how to create floating data points.

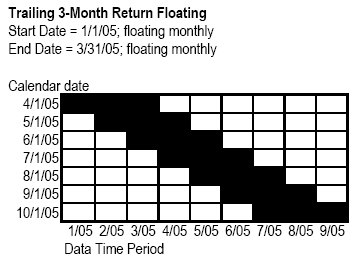

Trailing 3-Month Return Floating

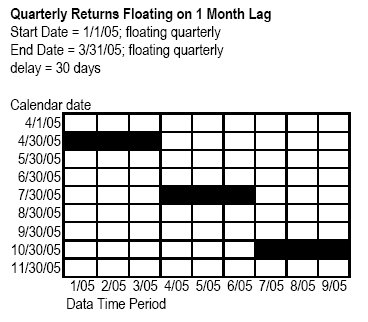

Quarterly Returns Floating on 1 Month Lag